The Spring Statement 2026 is primarily a fiscal and economic update, supported by the OBR’s latest forecast, rather than a full Budget with a broad package of new tax measures.

Snapshot Summary

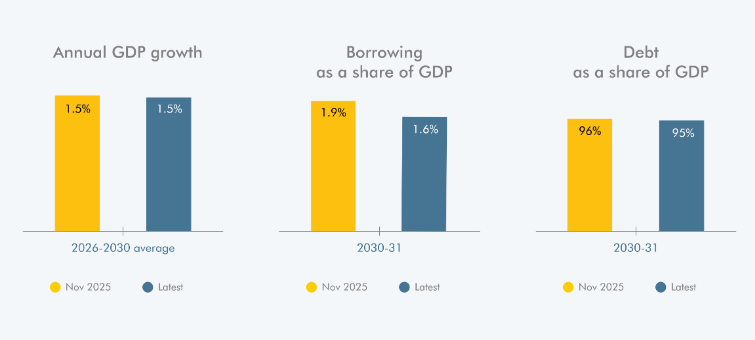

The OBR’s Spring 2026 forecast is an interim update ahead of the next Budget and keeps the overall picture broadly similar to November, but with weaker near term growth and a looser labour market. Real GDP growth is forecast at 1.1% in 2026 before averaging 1.6% across the later forecast years, while inflation is expected to return to the 2% target in late 2026.

Borrowing is still forecast to fall over the period, but public debt remains elevated at historically high levels. The OBR also highlights significant risks, including geopolitical instability, trade policy uncertainty, productivity weakness, labour market changes, and market volatility. For owner-managed businesses, this points to steady but cautious planning, strong cash discipline, and early preparation for future tax and policy changes rather than waiting for the next full Budget.

At Oldfield Advisory, we view this Statement through the lens of what matters to owner-managed businesses, families, and long term planning. While the government’s headline message focuses on stability, falling inflation and lower borrowing, the OBR’s underlying message is more balanced: progress in some areas, but a still challenging backdrop with material risks and uncertainty ahead.

To dive into more detail, you can download our focused summary of the Chancellor’s announcements and what they mean for you and your business.

Economic OutlookAt a glance

The OBR forecasts softer growth in the near term, with real GDP growth slowing to 1.1% in 2026 before improving in later years. Inflation is forecast to ease to target in late 2026, helped by lower food and energy inflation and a looser labour market. This is positive for business confidence, but not a signal to relax planning discipline, as demand conditions may remain uneven across sectors.

EmploymentThe OBR expects labour market conditions to loosen further in the near term, with unemployment rising before easing back later in the forecast. For employers, this may reduce some wage pressure over time, but payroll costs, recruitment quality, and productivity remain key planning priorities. Businesses should continue to review workforce structure, pay strategy, and output per role rather than relying on market conditions alone to improve margins.

Personal Tax and Family PlanningThis Spring Statement is not a major personal tax reset, but it reinforces the importance of proactive personal tax planning and family financial planning. The OBR continues to show a medium term fiscal path that relies heavily on higher receipts, with taxes as a share of GDP forecast to rise to historically high levels by the end of the forecast period. For business owners, this means salary, dividend, pension, and succession planning should remain under regular review rather than being left to year end decisions.

Business and FinanceBorrowing is forecast to improve gradually over the period, but public debt remains high and the OBR is clear that the outlook is sensitive to shocks, interest rates, equity markets, and productivity. For owner-managed businesses, the practical takeaway is to protect resilience: review financing arrangements early, stress test cashflow and covenant headroom, and avoid overcommitting based on one central forecast scenario.

Other matters:The OBR highlights significant risks around the current forecast, including conflict in the Middle East, global trade policy changes, productivity uncertainty, labour market outcomes, and market volatility. It also notes that this Spring forecast does not include a formal assessment of performance against the fiscal rules under the updated process, so the next Budget will remain the key event for further policy direction and fiscal rule assessment.

What owner-managed businesses should do now

- Reforecast cashflow for the next 6 to 12 months using cautious sales and margin assumptions

- Review borrowing facilities, renewal dates, and interest sensitivity

- Revisit pay, recruitment, and pricing strategy together, not in isolation

- Keep personal tax and extraction planning under regular review

- Prepare for further policy detail and potential tax changes at the next Budget

Download our detailed PDF to find out more about the Chancellor's announcements and what they mean for you.

_Page_1.jpg)

Tax affairs are complicated and we would always advise you speak with your advisers before making any changes. For more information on how we can help you and your business please contact us at info@oldfieldadvisory.com or call 02476673160.

Please note: This article is for general information purposes only and was correct as at the time of writing (03/03/26) and does not constitute financial advice. Statement proposals may be subject to change. You should contact us before taking any action as a result of the contents of this summary. Tax rules and legislation are subject to change, and their application depends on your individual circumstances. We recommend seeking advice from a suitably qualified tax adviser, and where relevant, an FCA-authorised financial planner. Any lists and details provided above are not exhaustive and are not intended to be full and complete guidance. No action should be taken without consulting detailed legislation or seeking independent professional advice. Therefore, no responsibility for loss occasioned by any person acting or refraining from action as a result of the material contained in this article can be accepted.

Share Article

You give us 30 minutes of your time. We'll give you growth and a plan

It's easy to book an initial consultation - just provide some brief details, and your preferred date and time, and we'll reply by email to confirm your appointment.

Contact us